Nexstar Broadcasting (NXST)

Date: December 2, 2016

Sector: Consumer Discretionary – Broadcast Media

Price/Market Cap: $59.2/$1.81B

Target/Implied Upside: $115/ 94%

[note: This is a write-up and update of research completed earlier in the year]

Thesis

Nexstar Broadcasting Group (NXST), a television broadcasting and digital media company, is in the early innings of both a company and industry-wide transformation. The company generates healthy free cash flow and trades at an attractive standalone valuation while also benefitting from strong growth in retransmission fee revenue. NXST expects to close a merger with Media General (MEG) by the end of the year, which will be immediately accretive and make NXST the second largest local television broadcasting company in the United States.

We believe the market has undervalued the potential for the company as it provides key localized content including local news and major sporting events which will remain valuable even as niche cable networks are squeezed out of cable bundles. Additionally, the company’s digital media products business is growing quickly and offers a diversified product portfolio for media publishers and advertisers.

Key Investment points:

- Focused on increasing revenue share (both profitability and reach) in owned stations while developing a growing portfolio of digital products and services.

- Diversified duopoly presence in multiple markets where they own broadcasting for programming of multiple networks. This broadens their addressable audience and allows for deeper demographic targeting. Each of the affiliates operates under consolidated physical facilities to reduce redundant costs.

- Localized sales force allows stations to leverage localized programming and community websites to target local advertisers.

- Invested in digital media technologies, which have created a growing portfolio of digital products and services currently reaching 115 million unique visitors for 848 million page views.

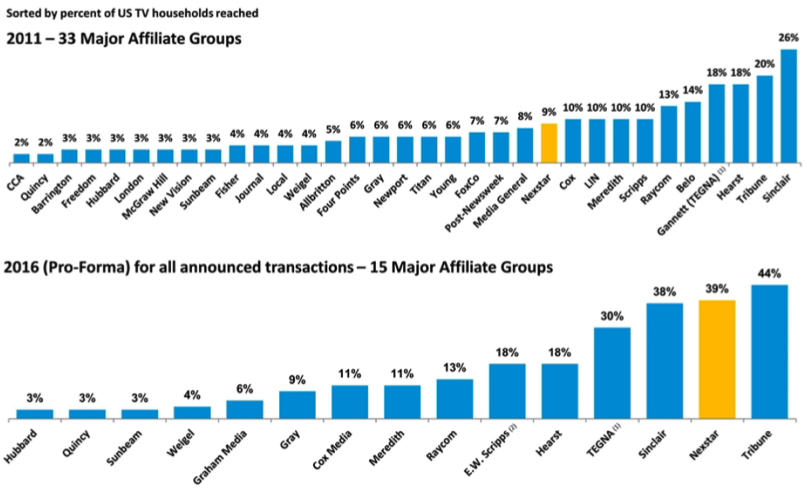

- Continued industry consolidation has decreased broadcast groups from 33 broadcasters in 2011 to 15 today. This trend is expected to continue to 6 mega-groups. And with the acquisition of smaller stations, larger stations are able to re-price retransmission fees creating immediate revenue leverage.

- Hidden spectrum value in the range of $11/share provides additional margin of safety.

Catalysts

- Merger Synergies – NXST management has a history of successful mergers. Management has indicated that they are well on track to achieve synergy goals with MEG that are expected to be $76m in year one and which will result in excess of 40% growth in annual pro forma free cash flow for 2016/2017 relative to current standalone FCF.

- Retransmission Pricing – Retransmission pricing has increased steadily for a number of years. With the increased scale post Media General merger, NXST will exert increased leverage in price negotiations with cable operators for content.

- Debt Reduction – Management has already indicated that interest expense for the combined entity will be $60m lower annually than original assumptions in their initial pro forma guidance.

- Incentive Auction – The FCC is currently conducting a Broadcast Incentive Auction, which will allow NXST to monetize certain spectrum assets. Management intends to reduce leverage (and associated interest costs), which is expected to be 5.5x 2-year trailing EBITDA at merger close. The sale of certain spectrum assets could potentially provide new opportunities for NXST M&A by clearing regulatory covenants.

Company

Consumer consumption habits are changing and customers now demand instant access to content anytime and anywhere. Customers once dreamed of a utopia of 500+ channels in their living rooms. However, the convergence of computing, mobile and gaming combined with a desire for customized, easily-digestible content has led to the delivery of TV Anywhere through skinny bundles or content purchased directly from providers. Nexstar Broadcasting is riding the wave of these industry trends and is poised to benefit as the market consolidates.

Nexstar owns, operates, programs, and provides sales and other services to 171 (post-merger) television broadcasting stations serving 100 markets, or 39% of all U.S. television households.

Business Model

Nexstar generates revenue from a combination of advertising, retransmission fees and digital media services. Television station revenue is primarily derived from the sale of local and national advertising. All network-affiliated stations are required to carry advertising sold by their networks, which reduces the amount of advertising time available for sale by stations. Nexstar’s stations then sell the remaining advertising to be inserted in network programming as well as the advertising in non-network programming. NXST retains all of the revenue received from these sales. Advertisers wishing to reach a national audience usually purchase time directly from the networks. National advertisers who wish to reach a particular region or local audience demographic often buy advertising time directly from local stations through national advertising sales representative firms. In these situations, the ability to address specific viewer demographics becomes increasingly valuable. Local businesses purchase advertising time directly from the station’s local sales staff.

Advertising rates are based upon a number of factors including:

- A program’s popularity;

- The number of advertisers competing for the available time;

- The size and demographic composition of the market served by the station;

- The availability of alternative advertising media in the market;

- The effectiveness of the station’s sales force;

- Development of projects, features and programs that tie advertiser messages to programming; and

- The level of spending commitment made by the advertiser.

Advertising rates are also determined by a station’s overall ability to attract viewers in its market area, as well as the station’s ability to attract viewers among particular demographic groups that an advertiser may be targeting. Advertising revenue is positively affected by national and regional political election cycles, and major events such as the Olympic games or the Super Bowl. Stations’ advertising revenue is generally highest in the second and fourth quarters of each year.

NXST also receives retransmission fees from cable, satellite and other multichannel video programming distributors (MVPDs) in their markets in return for consent to the retransmission of the signals of their television stations. The revenues primarily represent payments from the MVPDs and are typically based on the number of subscribers they have. Nexstar has been successful in negotiating agreements with MVPDs to produce meaningful sustainable revenue streams. As the company has increased scale, NXST has successfully renegotiated existing retransmission agreements on more favorable and profitable terms. SNL Kagan predicts gross industry retransmission growth to continue in the coming years.

In 2006, Nexstar began developing businesses related to digital media. These products provide digital publishing and content management platforms, a digital video advertising platform and other digital media solutions to media publishers and advertisers. The Company is focused on continued investment in new technologies and growing their portfolio of digital products and services complementary to their local news, entertainment and sports content. These products present opportunities for continued strong, organic growth.

Retransmission fees revenue and digital media represent the fastest growing business segments for NXST and, like their advertising, their digital media offerings are very localized in focus. This is in contrast to peers who develop their offerings to support creating national platforms.

(Source: company filings)

Local Focus

Nexstar focuses on medium-sized markets but consider themselves to be in the local media business. Each of the stations that Nexstar owns, operates, programs, or provide sales and other services to creates a highly recognizable local brand. Management estimates that in over 78% of the markets in which they produce local newscasts, they rank among the top two stations in local news viewership. As CEO Perry Sook states, “We are a local media business. We are in the business of creating and distributing local, relevant content […] and we help local businesses grow.” This is an important distinction as the television industry evolves. This local focus acts as a hedge against the prevailing industry trends of “cord cutting” where consumers are choosing to eliminate cable from their homes completely, “cord shaving” where consumers reduce the number of channels coming into the home or simply buy content directly from content creators. The advent of “skinny bundle” alternatives has left content creators scrambling for pipelines to get their content in front of consumers. Despite these trends, demand for local content remains strong.

Households will always be interested in knowing what is going on in their local neighborhoods and communities.

Strong local news typically generates higher ratings and enhances audience loyalty for programs both preceding and following the local news. Higher ratings also generate stronger advertising revenue from local advertisers. By focusing on local markets, NXST expects to continue to be a part of skinny bundles. As Sook commented, “We believe we are and will continue to be part of any skinny bundles. We have seen no material degradation in subscriber counts. […]We like our chances in a skinny bundle. We believe we will be on every skinny bundle going forward.”

Nexstar maintains a balanced portfolio of network affiliations including the Big Four: ABC, NBC, CBS and FOX affiliated stations which represented approximately 20%, 25%, 24% and 18%, respectively, of 2015 combined local, national and political revenue.

Market Consolidation

Nexstar is nearing completion of its proposed merger with Media General having already achieved DOJ and HSR approval and agreements to divest stations to meet ownership and regulatory approval covenants. The NXST/MEG combination is appealing in that big station groups with lucrative retransmission agreements with pay-TV operators can apply the terms of those agreements to the smaller stations they acquire, many of which have less favorable arrangements in place. The proposed merger is part of an ongoing industry trend, which has seen the broadcasting industry consolidate from 33 major affiliate groups in 2011 to 15 in 2016.

Sook envisions that 6 mega-groups will ultimately emerge, with Nexstar being one of the leaders. Since 2011, Nexstar has completed 17 accretive, strategic transactions including 60 full power TV stations and 4 digital businesses which have increased the company’s scale and diversified their revenue streams and broadcast portfolio. Post Media General acquisition, the combined companies will own 171 TV stations in 100 markets reaching 39% of all US TV households.

Spectrum

As the company has grown through acquisition, NXST has acquired spectrum assets whose value is not fully reflected on the balance sheet. Spectrum is the range of radio waves that can carry mobile signals including voice, image and data in digital format. TV Broadcasts, radio signals, GPS transmissions and cell phones all use spectrum to transmit bits of data over the air. Folk humorist Will Rogers was once quoted, “Buy land, they’re not making any more of it.” This same thought can be applied to the resource of electromagnetic spectrum, the real estate on which the wireless industry future will be built.

After years of planning, the FCC has begun auctioning the unused airwaves owned by TV broadcasters in what is called the Broadcast Incentive Auction. This spectrum will be reclassified for wireless use, becoming valuable real estate for mobile-phone carriers and others looking to enter the wireless-data business. Industry analysts expect the auction to bring in at least $30 billion, most of which will go to the TV-station owners who opt to participate. Nexstar has indicated that they plan to participate in the auction but information on auction results (which spectrum was sold and for what price) has not yet been publicly communicated. NXST has indicated they will use any proceeds from the auction to reduce debt. The sale of certain spectrum assets will also lift regulatory covenants allowing NXST to pursue additional acquisitions in certain markets. Of the major broadcast affiliate groups, Wells Fargo analysts rank Nexstar, Media General and Tribune Media as having the highest hidden spectrum values at $11, $4, and $3 per share respectively. This hidden value provides additional margin of safety for the investor.

Financial Performance and Valuation

Key Metrics:

| P/E ttm | 19.47x | Cash/Share | $1.35 |

| P/E Forward | 16.89x | ROA | 4.6% |

| P/FCF | 46.31x | ROI | 10.0% |

| PEG | 2.99 | ROE | 82.5% |

| P/BCF | 4.2x | Debt/EBITDA | 4.1x |

At December 31, 2015, the Company had NOLs of approximately $222.0 million for U.S. federal tax purposes and $105.8 million for state tax purposes.

The company is valued using a blended 2-year metric due to cyclical advertising spending related to political cycles. (i.e. Political ad spending increases every two years and using a blended two year average normalizes these fluctuations.) The Media General acquisition is scheduled to close before the end of the 2016 calendar year. Our valuation and multiples assume that the transaction is completed on time and the company achieves synergies projected by NXST management. As part of the transaction, management has agreed to divest 12 stations to meet ownership and regulatory approval covenants for an aggregate cash transaction value of $545m.

Peer company analysis:

M&A Precedents:

Broadcast television M&A precedents provide a more accurate view of normalized valuations. Within the industry, most acquisitions occur at an 8-10x trailing EBITDA multiple.

We set a target price of $115, which implies 93% upside. With the expectation of continued industry consolidation and increasing cash flow generation, we believe our valuation target could increase in the coming years.

Risks

- High debt levels – As of December 31, 2015, the Company had $1.5 billion of debt, which represented 94.8% of the total combined capitalization. The MEG transaction will add almost $4B in additional debt.

- Volatility in core advertising categories – In addition to the largest category of automotive, core advertising categories include retail, restaurants, telecom, insurance, and medical. Headwinds in these industries can pressure TV advertising demand and rates.

- Retransmission fee negotiations – While retransmission pricing has increased steadily for a number of years, there is uncertainty on how much additional leverage TV broadcasters have with MVPDs going forward. Negotiations can be contentious and sometimes lead to station blackouts.

- Over-the-top and skinny bundles – We may be underestimating the strength of the cord cutting momentum and the popularity of skinny bundles that exclude local broadcast stations and the Big 4 networks.

- FCC Risks – Any regulation or possible precursor to regulation that restricts affiliate broadcasters from effectively negotiating retransmission rates with MVPDs or limits/reduces their ability to operate jointly is a potential risk.

- M&A Risk – Problems with the integration of Media General or delay in deal closing poses a risk. The MEG deal is significantly larger than most deals NXST has completed.

Disclosures

The information contained herein reflects the opinions and projections of Richie Capital Group, LLC and its affiliates as of the date of publication, which are subject to change without notice at any time subsequent to the date of issue. Richie Capital Group does not represent that any opinion or projection will be realized. This information may not be reproduced, in whole or in part, without the written express consent of Richie Capital Group. The information on this site is protected under the applicable copyright laws in the US and other countries. Unauthorized retransmission, redistribution or other reproduction or modification of information contained in this site is prohibited and may be a violation of laws, including trademark or copyright laws and could subject the user to legal action. This is not a solicitation to buy or an offer to sell interest in our funds; such offers will be made only in compliance with applicable law. All information provided is for informational purposes only and should not be deemed as investment advice or a recommendation to purchase or sell any specific security. Additionally, this report is a summary version of our more detailed analysis and may not include key data points for investment decision. Richie Capital Group may or may not have an economic interest (long or short) in the price movement of the securities discussed in this presentation and Richie Capital Group’s economic interest is subject to change without notice. Our firm and/or clients may own shares or we may have previously acquired and divested our ownership position prior to publication. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. That wasn’t so hard was it? We tried to make it a bit shorter than the iTunes disclosure.

Leave a Reply