“Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold.” – Warren Buffett

From an investor’s perspective, 2018 was a challenging year that began with a strong first half, only to encounter a sharp reversal and decline. Looking back to the start of 2018, if we had known that we would end the year with no major military conflicts, a major tax cut, a revised trade deal with Canada and Mexico, 20%+ corporate earnings growth and unemployment at 3.7%[1], any rational investor would have predicted a strong market for 2018. The reality is that with the Republicans winning the White House in 2016 while already holding a majority of votes in The House and The Senate, the market expected legislation favorable to businesses and lower taxes. Expectations drove the market gains we saw throughout 2016 and 2017. The volatility we are seeing now….is based on investor expectations (and fears) for the year ahead.

Investors are clearly less upbeat than they were a year ago, and the fears are many:

- Slower earnings growth

- A possible recession

- Rising interest rates making bonds more attractive than equities

- Rising interest rates increasing the cost of buying a home

- Continued trade war with China

- Fading fiscal stimulus

- Legislative gridlock from a split Congress

- Impeachment rumblings

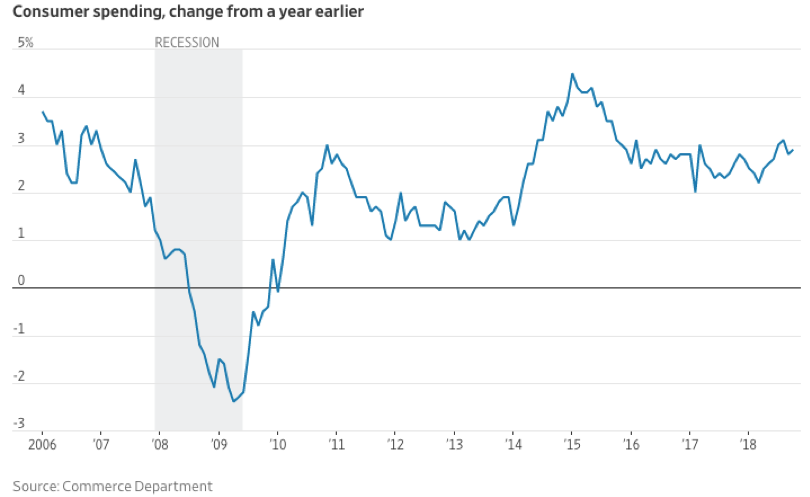

Investors smell a recession and are behaving accordingly. The global economy is slowing, but I do not believe a recession is imminent. The U.S. Economy remains stable having experienced 3% economic growth for two consecutive quarters. Employment figures for December highlighted 312k jobs being added. This number was well above the 180k jobs expected, and the largest monthly gain since February. Consumers have benefitted from a tight labor market, and consumers are still spending.

Market analysts expect earnings for S&P 500 companies to grow 7.8% in 2019, down from the previous forecast of 10.1%. Economists expect U.S. economic growth of 2.3% in 2019 and 1.8% in 2020[2]. This is slower than the 3.1% growth that was expected for 2018. But slowing growth does not equal a recession[3].

Interest Rates

December also saw The Federal Reserve raising interest rates for the fourth time this year. My view is that they are more than likely done with rate increases. The Fed has to strike a delicate balance between raising rates to tame inflation while not moving too fast and bringing economic growth to a halt. Slowing economic growth and possibly lower inflation should dissuade the Fed from raising rates this year. But as I have reminded certain clients, the recent rate increases are a healthy sign. We can’t have near zero percent interest rates forever. Rates this low fuel excessive risk taking and debt consumption. And when the economy is in real trouble, the Fed needs the ability to lower interest rates as a tool to boost the economy. On a historical basis, interest rates are still quite low.

(Graphic: 20-year Federal Funds Rate)

(Graphic: 20-year Federal Funds Rate)

What happens from here?

Consumers adjust to a “new normal”, and start buying houses with prices reflecting 4-5% mortgage rates as opposed to the 3-4% seen more recently. Prices adjust, followed by home buyers.

Trade War

The Trade War has played out as expected. All parties have suffered, even those not involved. The world is interconnected and tariffs are harmful to the global economy, not just Mexico, China or the European Union. The result has been a significant slowdown in global growth. China’s economy began to slow in the second half of 2018 with government-reported GDP growth that was the second lowest in the last 25 years. Chinese industrial production reached the lowest level since the Financial Crisis:

(Source: The Wall Street Journal)

(Source: The Wall Street Journal)

Over the last two decades, China’s role in the global economy has evolved. They are no longer just a manufacturer for the world. The country has become the largest market for many consumer, luxury, and durable goods. For many years, large U.S. multinational corporations have pointed to China as their primary market for growth. These companies will likely see their profit picture dim in the near term.

Here in the U.S., the impact of the trade war is best reflected through stories around the plight of soybean farmers. The trade war has closed off the Chinese market for many, and the cash price of soybeans has fallen by almost a third. To ease the pain, farmers have been given a $12B federal bailout, but most farmers would “rather just see trade than aid.”[4]

Technology stocks have been acutely affected because trade disputes amplify the interconnected global supply chain which technology companies rely upon for raw materials and manufacturing.

Does it get worse?

No. The trade war is over. Everyone lost. All economies have been harmed, and neither side has any significant bullets left to shoot. America and China have no choice but to reach a face-saving announcement which will likely be of little real change. Both countries can return home, declare “victory”, and restore the global trade engine. But even with a resolution, the Chinese market may be cut off for some companies as competitors have stepped in to fill the void during their absence.

Bottom Line

Aristotle once postulated plenism, or “horror vacui“– translated: “nature abhors a vacuum.” And as nature abhors vacuums, the market abhors uncertainty. The global and US markets do not look bad, but there is some uncertainty. This uncertainty is reflected in the volatility we have seen over the past quarter. Even some businesses leaders have become cautious as business investment growth fell to a 0.8% annual rate in September, down from 8.7% in the quarter prior. This is also a possible sign that corporate tax cuts are wearing off and the uncertain trade outlook is weighing on business decisions. Companies are slowing hiring and investment spending until there is more clarity on how global trade will affect their profits.

The bottom line is that the economy is still growing. Yes, it has slowed, but growing nonetheless. Inflation is under control. The Federal Reserve has interest rates where they want them. A split congress is not a horrible thing. Markets can perform well under gridlock as nothing will get done…. but nothing will get undone.

I have researched how markets react when there is a crisis in the White House. History does not paint a clear picture. The most obvious reference point is the Nixon presidency. However, during that time, the economy was already well into a recession from an oil price shock when the Watergate investigation began. Our Economy is much healthier. And the market barely paused its upward trajectory during the Clinton proceedings. A crisis would lead to more volatility but, in the end, investors would want to know as quickly as possible who would be setting direction for policies affecting trade, business and the economy. The faster those points are clarified, the faster the market will compartmentalize any Washington legal proceedings.

Psychologists Amos Tversky and Daniel Kahneman were pioneers in the creation of Behavioral Economics. Their work has taught us that investors feel losses (even temporary ones) about twice as much as equivalent gains. So, when markets are volatile and CNBC tickers are flashing nothing but red, our emotional instincts are immediately triggered. With some of our favorite stocks down 10%, 20% or even more, it doesn’t feel great. But it’s my job to remind you that our goal is to avoid emotional reactions, or complacency in the face of new data and facts. Investing is the only market where products go on sale and buyers get concerned. No one complains when cars, clothes, or homes are offered at a temporary discount. And it’s in down markets that investors have the opportunity to make their best gains. I expect us to do the same.

Being a long-term investor and thinking about the value of a company and what it will be worth in 5-10 years does not change very much day-to-day, month-to-month or even year-to-year. The long-term trajectory is the same. From that perspective, a company having a bad quarter (or year) is not that important.

We stay the course with our investment strategy.

Leave a Reply